Payment Optimization: what is it, and where do you start?

Payment optimization wasn't a phrase in most companies' lexicon, let alone an item on their roadmap, until fairly recently. That's changed as consumer purchasing behavior evolved and businesses recognized the importance of payments optimized for cost, performance, and customer experience.

Gone are the days when payments were an afterthought or an awkward inconvenience during the purchasing process. Today, they are a strategically vital aspect that can give businesses a competitive edge when properly optimized.

According to S&P's research, 45% of enterprise merchants have already recognized this opportunity and are actively working on optimizing their payments.

But what does optimizing payments mean? How do you optimize payments in your business? And what do you need to consider when working on a payments optimization project? This blog answers those questions.

What is payment optimization?

Payment optimization involves improving your payments strategy, technology stack, and processing logic to achieve several crucial objectives: reducing costs, improving authorization rates, minimizing instances of fraud, and providing a seamless customer experience.

These improvements can vary from minor adjustments, like rearranging payment methods at the checkout, to more significant changes, such as integrating new processors and implementing sophisticated orchestration strategies.

Given the complexity and diversity of the payments ecosystem, numerous options are available as you embark on your payment optimization journey. Success lies in understanding your business objectives and tailoring your optimization strategies to meet those needs.

Four key areas of payment optimization

Optimizing for conversion

The core purpose of your checkout page is to encourage customers to complete their payment. Getting this right is both art and science.

It's an art because you must ensure the look and feel of your checkout is on brand. It instills trust and provides a 'delightful' experience across all devices. This is foundational, and if you get it wrong, you'll find potential customers clicking elsewhere.

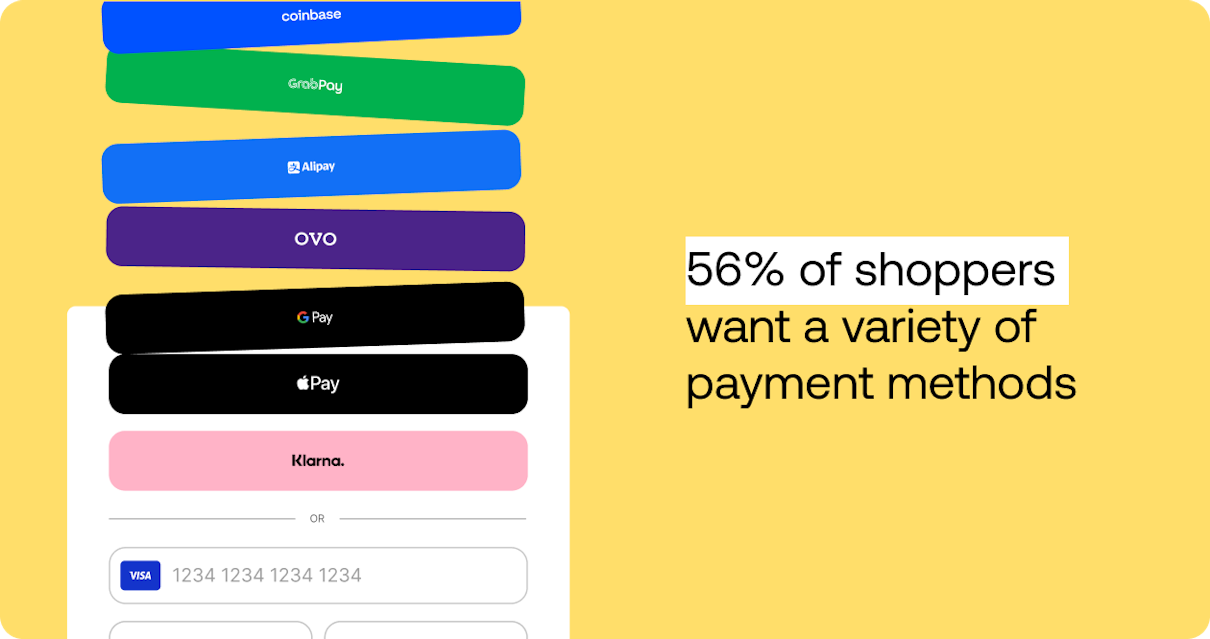

The science comes in when you consider your customers, where they are, and their preferences. For instance, if you're selling a watch to a customer in Hong Kong, offering a mix of cards and mobile wallets as payment methods and displaying the price in HDK would be essential. Similarly, when selling a different watch in Germany, it's advisable to provide payment options like SOFORT and GiroPay, and pricing the product in EUR.

These examples highlight just a few steps you can take to optimize your payments page. Remember that your customer's behavior is not static; as it evolves, so should your checkout. Regular testing and optimization are vital to maintaining high conversion rates.

Want to know what customers really want to see at the checkout? Get our report to find out.

Optimizing for authentication

In the era of Strong Customer Authentication in Europe and the growing adoption of 3D Secure globally, authentication has become a critical aspect of enhancing the safety and security of online commerce. However, this additional security measure has the potential downside of increased customer friction, leading to cart abandonment.

Optimizing authentication is a balancing act. And there isn't a one-size-fits-all approach to strike that balance; merchants must optimize based on their unique risk appetite and business objectives.

Thankfully, merchants have a range of tools at their disposal to strike this balance effectively. SCA regulations, for example, allow merchants to apply "exemptions," enabling certain payments to be processed without requiring customers to authenticate while still benefiting from the liability shift arrangement mandated by SCA.

Beyond Europe, the latest 3D Secure protocols introduce the concept of frictionless authentication. By leveraging additional customer information in the 3DS2 flow, merchants can identify scenarios where no further customer input is necessary to authenticate a payment.

We've taken this concept even further at Primer by developing an Adaptive 3DS solution. Our solution boosts conversion rates and simplifies the configuration process for determining when to prompt 3DS optimally. With Adaptive 3DS, customers are only asked to authenticate when it is absolutely required by the issuer, reducing unnecessary friction and potential cart abandonment.

Take a look at our Docs page to learn more.

Optimizing for authorization

Now things get complicated. Just because a customer has pressed pay—and maybe authenticated themselves— it doesn't guarantee the payment will be successful. Maybe your PSP will have an outage. Maybe the issuing bank will flag and stop the transaction. Or perhaps the customer doesn't have the funds in their account to complete the purchase. It's all possible.

While there's no foolproof solution to prevent these issues entirely, there are proactive steps you can take to mitigate their impact. Here are some examples for each scenario:

PSP outages: To safeguard your revenue, a backup or "fallback"processor is critical. This ensures that if your primary processor encounters a problem, transactions can seamlessly switch to the alternate processor automatically.

Issuing bank declines: When an issuing bank declines a transaction due to suspected fraud, you can attempt to recover the payment by asking the customer to authenticate using 3DS. The additional layer of authentication provided by 3DS can reassure the issuing bank and increase the likelihood of transaction approval.

Declines due to expired cards: Expired cards can be a common reason for payment declines, affecting businesses with recurring revenue models and those that store cards on file for faster checkout. If your business faces challenges with declined payments due to expired card credentials, consider using network tokens or an account updater solution.

These tips only scratch the surface. Get our playbook for growth mindset merchants for more.

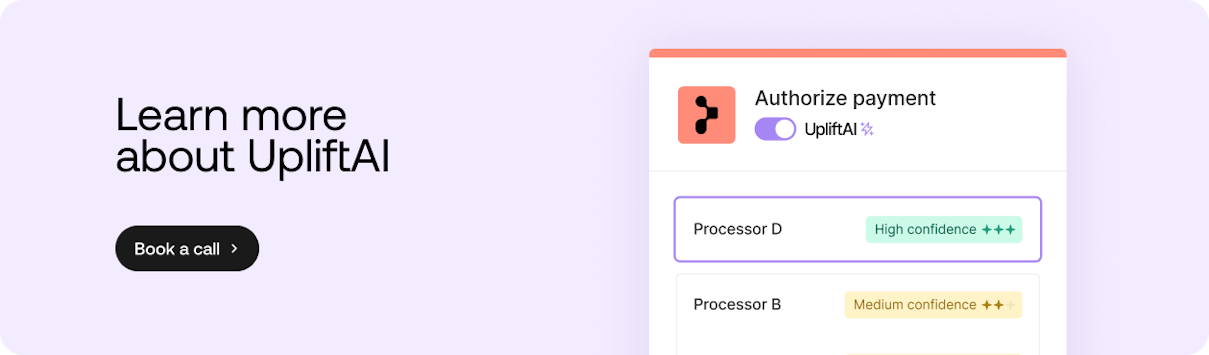

Use AI to boost authorization rates

AI For payments has arrived in the form of UpliftAI. Our AI-enabled smart routing solution provides merchants with as much as a 5% authorization rate uplift at the flip of a switch. Take a look at our blog introducing UpliftAI to learn more,

Optimizing for cost

Reducing the cost of accepting payments is a KPI for most payment teams. There are various strategies they can employ to achieve this goal:

Meeting minimum volume requirements: By reaching and maintaining the minimum transaction volume requirements set by payment service providers (PSPs), payment teams can unlock discounts. This means you can benefit from volume-based pricing, ultimately reducing the overall cost per transaction.

Fraud and chargeback reduction: Lowering instances of fraud and chargebacks is a critical step in cutting processing costs, fines, and fees. Implementing robust fraud prevention measures and adopting technologies like 3D Secure can help mitigate these risks, ultimately leading to cost savings.

Streamlining internal processes: Simplify your internal operations using automation tools for tasks like reconciliation. This not only eases the workload but also enhances accuracy and efficiency. Automated systems can improve accuracy and efficiency, resulting in cost savings over time.

While cost reduction remains a primary focus for merchants, it's crucial not to view payments solely as a cost center. The most successful and innovative businesses realize that payments are a powerful business enabler. You can unlock additional financial benefits beyond mere cost savings by implementing effective payment strategies.

Barriers to payment optimization success

Focusing on just one of these areas of optimization has the potential to unlock significant benefits for your organization. However, some blockers may hold your business back from realizing these benefits.

Little to no access to consistent and reliable data

Embarking on a payment optimization project requires a strong foundation, which includes benchmarking current performance and measuring the impact of changes. Having consistent and reliable data throughout your payment processes is vital. Yet, this can be challenging when dealing with multiple providers that structure data differently. At Primer, we've developed Observability, a solution that provides merchants with a consolidated and robust view of their performance across the entire payments ecosystem, overcoming this challenge.

Technical debt and resource constraints

Payment optimization often involves running several small tests to achieve incremental improvements. However, this approach becomes problematic when your business carries a heavy burden of legacy technical architecture, requiring significant resource investments even for minor changes. If your organization faces such constraints, assessing how to unlock flexibility in your payments stack is crucial before diving into any optimization initiatives.

Final thoughts

Payment optimization deserves the attention of every business. And it's essential to recognize that payment optimization isn't a one-time project; the payments ecosystem and consumer preferences are evolving. To stay ahead, optimizing payments should be an ongoing process, seeking to unlock marginal gains even when major projects take a back seat. This approach requires a payments infrastructure designed with flexibility at its core.

Find out how Primer's commerce infrastructure can deliver that for your business.