Fraud monitoring: best practices for detecting and preventing payment fraud

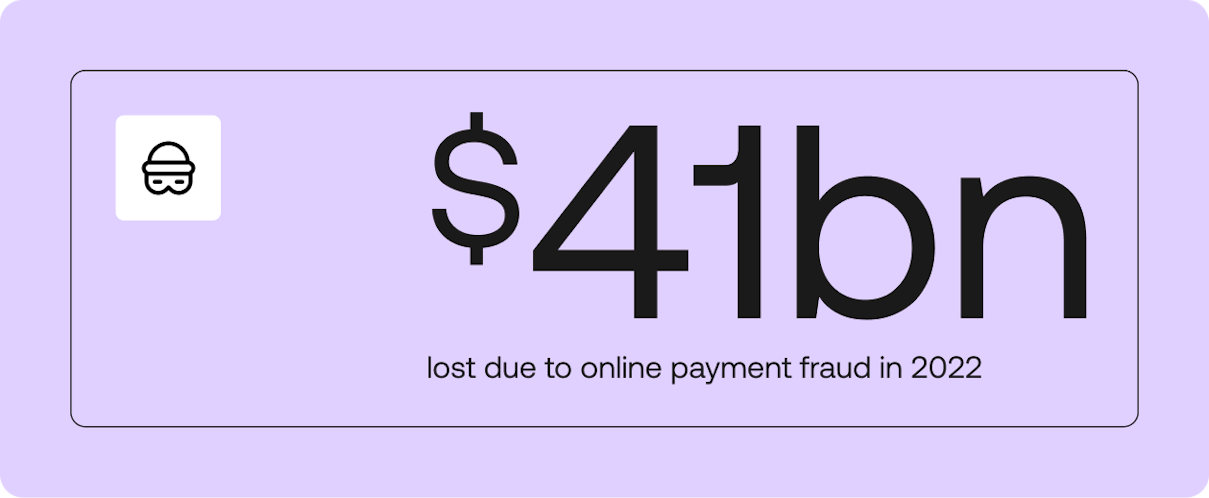

As the number of people paying online grows, so does the risk of fraud. In 2022, e-commerce losses to online payment fraud hit $41 billion. In 2023, it's expected to exceed $48 billion. It’s also projected that online sellers could face losses surpassing $206 billion from 2021 to 2025.

But the consequences do not stop there. Customer trust, brand reputation, and financial stability are all on the line. This is without even considering the long-term value lost from customers, the impact on the brand, and the possibility of fines.

Because of these far-reaching consequences, the detection and prevention of payment fraud have become paramount for all businesses. This article will explore the most effective methods businesses employ to monitor and stay ahead of fraudsters.

There are many ways fraudsters can commit online payment fraud. Here are some of the most common forms:

Credit card fraud is the unauthorized use of someone's credit card information for purchases or withdrawals. For example, fraudsters may steal card details from compromised websites and make online purchases without the cardholder's consent.

Card testing fraud is where cybercriminals validate stolen credit card information by conducting small, inconspicuous transactions before attempting larger ones.

Account takeover fraud happens when a fraudster gains unauthorized access to someone's online accounts (e.g., email, banking, e-commerce) to conduct fraudulent transactions or access sensitive information.

BIN attacks involve cybercriminals employing brute-force methods to deduce valid credit card details, including the card number, expiration date, and card verification value (CVV). Once they crack the code, they initiate card testing – executing small transactions to confirm the card's viability for illicit purposes.

Friendly fraud, also known as chargeback fraud, happens when a legitimate cardholder makes an online purchase but later disputes the charge with their bank or credit card company, falsely claiming they didn't receive the goods or services.

Refund fraud exploits return policies to obtain illegitimate refunds. For instance, a fraudster buys an expensive item, uses it briefly, returns a counterfeit or cheaper version, and sells the authentic item for profit, causing a loss to the merchant.

Gift card fraud encompasses various tactics used to steal the value of gift cards. For instance, criminals may tamper with gift cards in stores, secretly recording the activation codes and later using that information to drain the card's value before the rightful recipient can use it.

What is fraud monitoring?

Fraud monitoring is a crucial part of stopping fraud. It's about what businesses do to find and prevent possible fraud. This involves keeping a close watch on customer payments and user behavior.

When businesses take a proactive approach to fraud monitoring, they use different tools to spot risks. They may build these in-house or leverage specialist platforms from companies like Riskified, Forter, Sift and Signifyd. These fraud monitoring solutions leverage real-time data from online sessions, devices, IP addresses, and user behavior to assess risk and make decisions based on rules set by the user and, increasingly, artificial intelligence.

See how Observability Monitors & Alerts empower merchants to stay on top of their payment data.

How to detect payments fraud

Detecting fraud before or during a transaction is critical to safeguarding users and businesses. Here are a few of the fraud indicators businesses should look out for:

False information being provided. For example, suspicious-looking phone numbers or email addresses

Inconsistent customer details used across different purchases

Unusually large orders made, like several of the same items or exclusively the most expensive products

Multiple payment cards used with the same shipping address

An excessive number of payments made from the same card from different IP addresses

Multiple declined transactions made with different cards

Requests to split a large order into multiple payments on different cards

How to prevent payments fraud

Securing online payments requires a multi-faceted approach. Tools merchants can use include:

Managing user accounts

Businesses have various tools at their disposal to counteract fraudulent activities during the registration process and subsequent log-ins. These tools include email verification, CAPTCHA challenges, phone number confirmation, analysis of IP addresses, detection of unusual login patterns, and device fingerprinting. Additionally, businesses can implement two-factor authentication (2FA), passwordless authentication, or even magic email links to enhance security.

AVS

Address Verification Service (AVS) cross-references the transaction billing address with the card issuer's records to detect suspicious activities, especially in online purchases. Misalignment raises an immediate red flag.

CVV

Card Verification Value (CVV) is the security code on the back of credit and debit cards. When customers make purchases, they must input this three or four-digit code. This additional security measure ensures that the user physically possesses the card. Requiring CVV helps stop fraud by unauthorized individuals who may have stolen card information but lack the CVV code.

3D Secure

The 3DS protocol requires customers to meet the Secure Customer Authentication criteria. They will need to authenticate using two of the following:

Something the customer is - e.g., a fingerprint

Something the customer has - e.g., a mobile device

Something the customer knows - e.g., a password

Use tools from a specialist fraud provider

By partnering with a fraud provider, you’ll benefit from specialist software designed to enhance security and prevent fraud. As these are agnostic, merchants can flow their entire transaction volume through the solution and provide a more comprehensive level of protection. These tools also offer a growing range of risk management solutions beyond payments or that are payments adjacent.

You can connect with multiple different fraud providers through Primer. Learn more.

Link analysis

Link analysis examines the complex network of relationships among entities. It uncovers hidden connections and patterns that would otherwise remain undetected by traditional monitoring methods.

By tracing the flow of funds, commonalities among fraudulent accounts, and scrutinizing transactional behavior, link analysis enables fraud detection teams to respond swiftly to potential threats.

Take advantage of AI and machine learning

Artificial intelligence (AI) and machine learning have sparked considerable business interest. Supervised machine learning, for example, can be used to recognize patterns in fraudulent transactions and flag suspicious behavior in real-time.

In addition, organizations can leverage unsupervised machine learning to unveil concealed patterns hidden within extensive datasets that elude human observation. Moreover, applying Natural Language Processing (NLP) enables the analysis and interpretation of unstructured data.

The ongoing battle against fraud is akin to an arms race. As fraudsters continually refine their tactics, it becomes imperative for your systems to evolve in parallel. Hence, adopting AI and machine learning is no longer an optional luxury but an absolute necessity.

Immerse yourself in fraud trends

Regularly analyzing data, studying industry reports, and staying updated on evolving tactics sharpens the ability to recognize warning signs and potential vulnerabilities. Embracing this proactive approach is the key to staying ahead of fraudsters.

How does fraud monitoring improve the customer experience?

Showing a strong dedication to security by using effective fraud monitoring builds trust and confidence with customers.

For example, using biometric authentication like fingerprints or facial recognition offers easy authorization. It also removes the necessity for complicated passwords or lengthy verification steps. Consequently, your customers experience convenience and quicker payment processing.

How to choose a payment fraud prevention solution

When researching fraud prevention solutions and tools, there are several considerations. You’ll want to ensure the solution/s you choose will effectively support your fraud monitoring efforts and reduce risk.

Some things you’ll want to think about include:

Fraud prevention objectives

Budget

Features and capabilities

Solution customizability

Integration process

In addition to these considerations, you should ask yourself some important questions.

Does the solution use a wide variety of data?

The solution you select should use various data to inform the risk decision-making process. This should include transaction details, chargeback information, and other supporting data. This data is essential for analysts to review potential fraud risks from every angle.Does the solution use machine learning?

Tools and solutions that use a combination of machine learning and manual review are better equipped to adapt to new fraud patterns and continuously identify and learn from them.Can the solution make real-time decisions?

With more strict rules for fraud detection in place, your rate of false positives could increase. Tools that can make real-time transaction decisions will balance the customer experience and fraud prevention, helping you reduce payment challenges for legitimate customers.

The bottom line

Monitoring fraud and using the best methods to detect and prevent payment fraud is essential for safeguarding businesses and customers.

With technological advances happening all the time and fraudsters becoming more advanced in their approach, the fight against fraud continues. This requires constant adaptation and proactive strategies from every type of business. By following the guidelines presented in this article, you can be empowered to strengthen your defenses and ensure the security and reliability of online transactions for everyone involved.